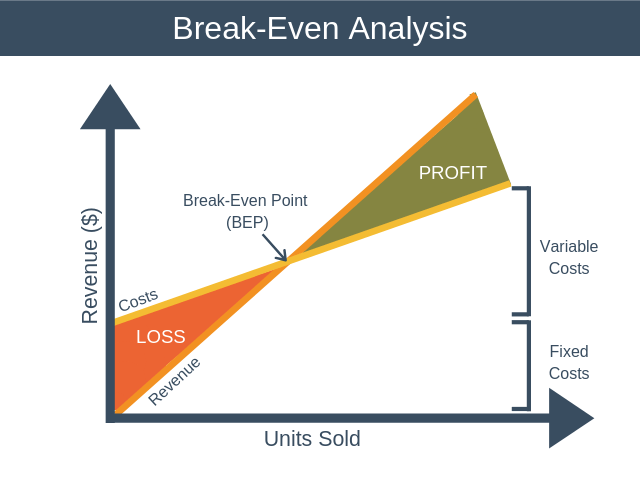

The term “Break-Even Point” refers to the level of sales necessary to cover all expenses i.e. the point of no profit or loss. To calculate this, you need the following:

- Your expenses

- Your sales

- Your gross profit percentage which is your gross profit (sales less your cost of sales) expressed as a percentage of your sales

Your break-even point is calculated by dividing your total expenses by your gross profit percentage and then multiplying by 100/1 e.g. if your sales are $180,000 and your gross profit $90,000, your gross profit percentage would be 50%. Your expenses are $60,000.

| Expenses | $60,000 | |

| Gross profit percentage | 50% |

Total costs divided by 50 $1,200

Multiplying this by 100/1 equals the break-even sales of $120,000

Things to bear in mind:

- Just breaking even means that there is no return on investment for you as business owner, so add the required net profit to your expenses to give you a more realistic break-even point.

- Variable costs. Not all expenses are fixed e.g. if your sales vary your business expenses may also vary.

- Proprietor’s costs. Your expenses may exclude remuneration for you as business owner which needs to be adjusted for if you want any drawings from the business!

Every business owner should know what the fixed costs and unavoidable variable costs are for them to open their doors and should be aware of their gross profit so that the break-even point at that level of operations can be determined. Once you know this information this will enable you to monitor your actual sales performance as against your break-even figure so you know what sales you have to achieve.